Finance & Banking

Want to Start a Family One Day? Take These 10 Financial Steps Now

:max_bytes(150000):strip_icc():format(jpeg)/GettyImages-592016191-516657cb0b9044098276f9c30889afb3.jpg)

As you and your accomplice take into consideration rising your loved ones, it’s necessary to acknowledge that your priorities and monetary targets will change. Having a baby is among the most financially vital milestones a household will expertise, and it’ll doubtless change the trajectory of your monetary plan shifting ahead.

That being stated, there are steps you may take now to assist put together for the journey forward, from contemplating the medical prices to starting a college fund, and nearly every thing in between.

Listed here are 10 key monetary steps to take now to arrange for the life adjustments that include rising your loved ones.

Key Takeaways

- Perceive what being pregnant and childbirth care your medical insurance covers, and be ready for out-of-pocket prices like deductibles, copays, and providers that may not be included in your plan.

- The U.S. doesn’t mandate paid parental go away, which means you must evaluate your FMLA go away eligibility and discover different advantages your employer could supply.

- Open an schooling financial savings account, reminiscent of a 529 plan, to profit from tax benefits and long-term compounding, even in case you begin with small contributions.

- Replace your property plan to make sure your baby and their inheritance are cared for in your absence.

Table of Contents

1. Assessment Your Well being Protection

When you’ve got health insurance, examine along with your supplier to see what prenatal care is roofed and what you’ll be anticipated to pay out-of-pocket. Medically crucial prices referring to the being pregnant and delivery should be coated by most medical insurance plans, however further providers will doubtless be at your personal expense.

Take into accout, simply because a service is “coated” by your supplier doesn’t imply you gained’t be paying for it. Generally, you’ll nonetheless be required to pay for many providers till your annual deductible has been met, or if a copay or coinsurance is required.

In just a few states, being pregnant confirmed by a medical skilled can rely as a qualifying life event for a particular enrollment interval. In any other case, you’ll want to attend till the newborn is born to alter your plan or get hold of protection via a particular enrollment interval (in case you don’t have medical insurance). Uninsured people can examine for eligibility via Medicaid or CHIP, each of which elevate the earnings limits for pregnant girls (making it simpler for extra people and households to qualify).

2. Plan for Household Depart

Whereas the USA doesn’t have federally mandated paid parental go away, eligible workers might be able to use Family and Medical Leave (FMLA) to take as much as 12 weeks of protected, unpaid time from work.

Test in case your employer affords any paid parental leave or if you should use accrued trip or sick days. Short-term disability advantages might also assist bridge the hole. The bottom line is planning forward for any interval of unpaid day without work.

As a result of paid day without work just isn’t a assure, you’ll want to think about how a pay hole will impression your monetary well-being. In preparation, you might must set extra apart in savings, for instance, and communicate to your employer about your choices.

3. Plan for Child Bills

There’s no denying it, babies are expensive and so they require a lot of equipment. When you might be able to offset some prices with the assistance of a child bathe or presents from family members, you’ll nonetheless must plan to purchase fairly a bit in preparation on your child’s arrival (and within the months following their delivery as effectively).

Some high-ticket objects may embody:

- Components

- Diapers

- Stroller

- Crib and mattress

- Automotive seat

- Excessive chair

- Child garments

Sooner or later, you’ll additionally want to think about further prices like childcare, child meals, child gates and different security tools, toys, and making contributions to a college savings fund.

4. Plan for Childcare

Childcare, other than insurance coverage and medical payments, will doubtless be one in all your highest prices related to beginning a household. Your choices for childcare differ vastly, relying on the place you’re positioned, your loved ones standing, and your targets or priorities. That being stated, the common annual cost of childcare in America for infants is round $17,171, over 19% of a median household’s earnings.

Contemplating the price of childcare can simply exceed a household’s hire or mortgage fee, it’s price contemplating your most life like plan of motion. When you’ve got mother and father or different family members close by who need to assist out, this could actually cut back the associated fee (even when they watch the kid for simply in the future every week).

When you plan on leaving the workforce to remain dwelling along with your baby completely, contemplate how a drop in household income will impression your skill to deal with your new monetary obligations and ongoing long-term targets (like retirement financial savings or homebuying).

5. Create an Emergency Fund

Everybody ought to have an emergency fund, however it turns into more and more necessary when you put together to start out a household. Proper now, it’ll be arduous to foretell precisely how your monetary state of affairs will change.

You may estimate your medical bills and value out child tools, however in the end, you need to put together for the sudden. This might embody a sudden job loss, automobile repairs, the necessity to purchase an even bigger dwelling prior to anticipated, an financial downturn, or perhaps a set of twins.

6. Plan to Get a Social Safety Quantity for Your Youngster

Your new child will want a Social Security number. You may point out that you just’d like to use on your baby’s Social Safety quantity when you full the delivery registration paperwork within the hospital.

As soon as the Social Safety Administration assigns your baby a quantity and mails out an official Social Safety card, you should use that to do issues like apply for medical insurance for the kid and open a bank account of their identify.

7. Replace your Life Insurance coverage and Incapacity Insurance coverage

When you’ve got insurance coverage insurance policies, they’ll have to be up to date to replicate your altering household standing.

Think about whether or not your current life insurance, for instance, affords sufficient protection to deal with the wants of your surviving partner and baby (or kids). This might embody massive bills just like the mortgage funds and utilities, childcare, faculty tuition, and future school prices.

Chances are you’ll be enrolled in your employer’s group life or disability insurance already. If that’s the case, communicate to your employer about buying further protection or discovering a separate coverage that higher fits your wants.

8. Open a Financial savings Account for Schooling

The price of school continues to rise, and in case you’d like to assist offset your baby’s future academic prices, now’s the time to start out saving. As quickly as you’re ready, open an education-focused financial savings or investment account, and begin setting apart what you may (whereas nonetheless maintaining along with your different monetary priorities and long-term financial savings targets).

A 529 plan is a state-sponsored financial savings plan particularly designed to assist households save for academic bills in a tax-advantaged method, since withdrawals could also be tax-free if used on qualifying bills.

You can too set up a Uniform Transfers to Minors Act (UTMA) or Uniform Gifts to Minors Act (UGMA) account, which offers extra spending flexibility on your baby as soon as they change into a authorized grownup (although these accounts don’t include the identical tax benefits).

9. Replace Property Planning

After getting a baby, your estate planning paperwork will have to be up to date. In your will, for instance, you need to designate a legal guardian within the occasion you and your partner die. You can too add your baby as a beneficiary of your property. You may additionally need to contemplate figuring out one other member of the family or a trusted particular person as a trustee of your baby’s inheritance, do you have to die whereas they’re nonetheless a minor.

When you’ve got a financial power of attorney, replace it to make sure your chosen particular person could make monetary selections on your baby within the occasion you change into incapacitated as effectively.

Vital

You’ll doubtless must work with an lawyer when updating your property plan to make sure all facets of your monetary life are thought-about and accounted for.

10. Begin Saving for Future Bills

Maybe a very powerful step you may take is to start saving now for future bills, together with people who really feel impossibly far down the street. Not solely will you incur bills through the being pregnant and childbirth, however you’ll want to think about issues like greater healthcare prices, day without work work (particularly if one partner is leaving their job for good), and childcare prices—along with your different recurring monetary obligations and payments.

You’ll additionally must bear in mind the chance of inflation and the impression rising costs can have in your bills over time. The extra you’re in a position to put aside now, the extra ready you’ll be to deal with the sudden and ongoing prices of getting a baby.

The Backside Line

As you contemplate the logistics of getting a baby, don’t underestimate simply how a lot your loved ones’s funds will change. From prenatal care into infancy and up via school, it may simply price hundreds of {dollars} every month to offer every thing your loved ones must proceed rising and thriving.

Begin saving early, leverage the ability of compounding earnings, and maintain your safety plans up-to-date to make sure your loved ones is well-cared for now and sooner or later.

Finance & Banking

Today’s Lowest Refinance Rates by State

:max_bytes(150000):strip_icc():format(jpeg)/4-AfloImages-da6e5bc6b6104a7cab3dbaed5e28caaa.jpg)

The states with the most affordable 30-year mortgage refinance charges Tuesday had been New York, California, Texas, Washington, Connecticut, Florida, New Jersey, and Pennsylvania . The eight low-rate states registered refi averages between 6.99% and seven.11%.

In the meantime, the states with Tuesday’s costliest 30-year refinance charges had been West Virginia, Kansas, Hawaii, Idaho, Missouri, North Dakota, and Wyoming. The vary of 30-year refi averages for the highest-rate states was 7.23% to 7.26%.

Mortgage refinance charges range by the state the place they originate. Completely different lenders function in several areas, and charges could be influenced by state-level variations in credit score rating, common mortgage measurement, and rules. Lenders even have various danger administration methods that affect the charges they provide.

Since charges range extensively throughout lenders, it is all the time sensible to buy round for your best mortgage option and evaluate charges commonly, regardless of the kind of house mortgage you search.

Nationwide Mortgage Refinance Fee Averages

Charges for 30-year refinance mortgages fell 4 foundation factors Tuesday, reducing the common to 7.17%—an enchancment vs. a Might peak of seven.32% that was a 10-month excessive. Charges are actually right down to their lowest stage in three weeks.

Again in March, nonetheless, charges sank to a 6.71% common, their least expensive 2025 mark. And final September, 30-year refinance charges plunged to a two-year low of 6.01%.

| Nationwide Averages of Lenders’ Greatest Mortgage Charges | |

|---|---|

| Mortgage Sort | Refinance Fee Common |

| 30-Yr Fastened | 7.17% |

| FHA 30-Yr Fastened | 7.58% |

| 15-Yr Fastened | 5.95% |

| Jumbo 30-Yr Fastened | 7.10% |

| 5/6 ARM | 7.10% |

| Provided via the Zillow Mortgage API | |

Watch out for Teaser Charges

The charges we publish gained’t evaluate instantly with teaser charges you see marketed on-line since these charges are cherry-picked as probably the most enticing vs. the averages you see right here. Teaser charges could contain paying factors upfront or could also be primarily based on a hypothetical borrower with an ultra-high credit score rating or for a smaller-than-typical mortgage. The speed you in the end safe shall be primarily based on components like your credit score rating, revenue, and extra, so it might probably range from the averages you see right here.

Calculate month-to-month funds for various mortgage situations with our Mortgage Calculator.

What Causes Mortgage Charges to Rise or Fall?

Mortgage charges are decided by a fancy interplay of macroeconomic and trade components, similar to:

- The extent and path of the bond market, particularly 10-year Treasury yields

- The Federal Reserve’s present financial coverage, particularly because it pertains to bond shopping for and funding government-backed mortgages

- Competitors between mortgage lenders and throughout mortgage sorts

As a result of any variety of these may cause fluctuations concurrently, it is usually tough to attribute any change to anybody issue.

Macroeconomic components stored the mortgage market comparatively low for a lot of 2021. Specifically, the Federal Reserve had been shopping for billions of {dollars} of bonds in response to the pandemic’s financial pressures. This bond-buying policy is a significant influencer of mortgage charges.

However beginning in November 2021, the Fed started tapering its bond purchases downward, making sizable month-to-month reductions till reaching internet zero in March 2022.

Between that point and July 2023, the Fed aggressively raised the federal funds rate to battle decades-high inflation. Whereas the fed funds charge can affect mortgage charges, it would not instantly achieve this. In truth, the fed funds charge and mortgage charges can transfer in reverse instructions.

However given the historic pace and magnitude of the Fed’s 2022 and 2023 charge will increase—elevating the benchmark charge 5.25 share factors over 16 months—even the oblique affect of the fed funds charge has resulted in a dramatic upward affect on mortgage charges over the past two years.

The Fed maintained the federal funds charge at its peak stage for nearly 14 months, starting in July 2023. However in September, the central financial institution announced a first rate cut of 0.50 share factors, after which adopted that with quarter-point reductions on November and December.

For its third assembly of the brand new yr, nonetheless, the Fed opted to hold rates steady—and it’s potential the central financial institution could not make one other charge lower for months. With a complete of eight rate-setting conferences scheduled per yr, which means we may see a number of rate-hold bulletins in 2025.

How We Monitor Mortgage Charges

The nationwide and state averages cited above are offered as is through the Zillow Mortgage API, assuming a loan-to-value (LTV) ratio of 80% (i.e., a down fee of at the least 20%) and an applicant credit score rating within the 680–739 vary. The ensuing charges symbolize what debtors ought to count on when receiving quotes from lenders primarily based on their {qualifications}, which can range from marketed teaser charges. © Zillow, Inc., 2025. Use is topic to the Zillow Phrases of Use.

Finance & Banking

Americans Are Vacationing This Summer, But Tariff Worries Mean They’re Cutting Costs

:max_bytes(150000):strip_icc():format(jpeg)/GettyImages-1996332692-cb2f0a606d314c859b6455fdd94c1a98.jpg)

KEY TAKEAWAYS

- Whereas President Donald Trump’s tariffs and inflation uncertainty hasn’t stopped individuals from planning holidays, it has influenced many shoppers to chop prices.

- Extra vacationers are adjusting their plans to include cheaper housing and journey.

- Many are additionally planning to combine work and leisure for an extended journey.

The vast majority of People are desirous to take a summer season trip this 12 months, even when they need to plan a less expensive journey to regulate for potential tariff-related inflation.

Journey charges have continued to hit record highs after COVID-19 pandemic restrictions lifted years in the past. The truth is, journey is up by 19% since 2022, and about half of shoppers say journey is extra very important now than it was 5 years in the past, in accordance with a survey by Expedia Group.

Nonetheless, President Donald Trump’s back-and-forth tariffs have worried many consumers, who’re uncertain of their financial affect. But even with a lot uncertainty, 88% of shoppers are nonetheless planning a trip, Expedia discovered.

Journey Is A Precedence, However So Is Reducing Prices

Whereas shoppers are nonetheless prepared to spend cash on on a summer season journey, nearly six in 10 shoppers count on to be extra price-conscious whereas touring this 12 months, in accordance with Expedia Group.

A March Deloitte survey discovered that vacationers deliberate to spend 21% extra on journey this summer season than final 12 months. Nonetheless, that quantity shrank to 13% when shoppers had been surveyed in April, the month Trump’s widespread tariffs went into effect.

“Vacationers seem desirous to embark on their summer season journeys, however pricing pressures and financial influences are anticipated to chart the course for the way they get there,” mentioned Kate Ferrara, vice chair and U.S. transportation, hospitality and companies sector chief for Deloitte, in a press launch. “By swapping flights for street journeys or planning shorter, budget-friendly adventures, vacationers are possible in search of worth whereas making reminiscences.”

To attain budget-friendly holidays, extra vacationers are favoring shorter, extra frequent escapes over one huge journey. As well as, 33% are planning to remain at finances resorts, 30% will stick with household and pals, 20% will decide cheaper airfare, and 22% will drive as an alternative of fly, in accordance with Deloitte.

Many are additionally mixing work journeys with leisure for a less expensive “bleisure” or “flexcation” journey, in accordance with Expedia Group. This 12 months, nearly 1 / 4 of vacationers plan on working remotely whereas on trip. Compromising on this method has allowed more and more extra vacationers the chance to take longer journeys to worldwide locations, in accordance with Deloitte.

Finance & Banking

DR Horton, Wells Fargo, Dollar Tree, and More

:max_bytes(150000):strip_icc():format(jpeg)/GettyImages-2201316575-76516c536af54ded9eb06f2ed6f93a1b.jpg)

Key Takeaways

- U.S. equities had been barely greater at noon as a brand new report on non-public sector hiring missed estimates, sending bond yields down.

- Shares of D.R. Horton and rival homebuilders gained on the drop in Treasury yields and a brand new name from President Donald Trump for the Federal Reserve to decrease rates of interest.

- Tesla gross sales in three massive European markets fell.

U.S. equities had been barely greater at noon as a weaker-than-expected non-public sector employment report despatched bond yields tumbling. The Dow Jones Industrial Average, S&P 500, and Nasdaq had been all greater.

Shares of D.R. Horton (DHI) and different homebuilders superior on the falling borrowing prices and President Donald Trump’s renewed name for Federal Reserve Chair Jerome Powell to slash rates of interest.

Thor Industries (THO) shares rose when the leisure automobile (RV) maker beat revenue and gross sales estimates on greater North American demand and its effort to scale back bills.

Wells Fargo (WFC) shares had been up because the Fed lifted the asset cap it slapped on the financial institution seven years in the past following a collection of scandals.

Greenback Tree (DLTR) was the worst-performing inventory within the S&P 500 after the low cost retailer warned its current-quarter revenue may take a 50% hit due to prices from new U.S. tariffs.

Shares of CrowdStrike Holdings (CRWD) slid when the cybersecurity agency gave weak steering because it continues to really feel the fallout from its glitch that led to a worldwide IT outage final yr.

Tesla (TSLA) shares declined when gross sales of the carmaker’s EVs fell in Britain, Germany, and Italy final month.

Oil futures fell. Gold costs rose. The U.S. greenback misplaced floor to the euro, pound, and yen. Main cryptocurrencies had been combined.

TradingView

What Fleet Managers Need to Know to Keep Drivers Safe

This publish is a part of a collection sponsored by IAT Insurance coverage Group. For companies that depend on fleet...

JPMorgan to Accept Bitcoin ETFs as Collateral Globally

JPMorgan is reportedly getting ready to simply accept bitcoin ETFs as collateral for loans globally, signaling a groundbreaking shift towards...

Want to Start a Family One Day? Take These 10 Financial Steps Now

As you and your accomplice take into consideration rising your loved ones, it’s necessary to acknowledge that your priorities and...

Trump administration moves to pull funding on high-speed rail

The Trump administration discovered “no viable path” ahead to finish California’s high-speed rail venture following an almost four-month investigation that...

Today’s Lowest Refinance Rates by State

The states with the most affordable 30-year mortgage refinance charges Tuesday had been New York, California, Texas, Washington, Connecticut, Florida,...

15 Essential Tips Before Visiting a Car Dealership in Alabama

Many Alabama residents equate a trip to the car dealership with a trip to the dentist. You have to do...

Finys hires Norman as Chief Growth Officer, Khetrapal as Director of Finance

Finys, an insurance coverage software program options supplier headquartered in Troy, Michigan, appointed Tim Norman as chief progress officer and...

Venmo introduces new debit card benefits and payment options as rival Cash App struggles

Venmo goals to be extra than simply an app for paying buddies with its newest update. On Wednesday, the PayPal-owned...

Americans Are Vacationing This Summer, But Tariff Worries Mean They’re Cutting Costs

KEY TAKEAWAYS Whereas President Donald Trump’s tariffs and inflation uncertainty hasn’t stopped individuals from planning holidays, it has influenced many...

10 Simple Ways to Spread the Optimism and Positive Energy Starting Today

“A pessimist sees the problem in each alternative; an optimist sees the chance in each issue.”Winston Churchill Optimism. It may...

Where Is Tom Girardi Now? His Life 5 Years After Fraud Scandal

NEED TO KNOW In 2020, famed lawyer Tom Girardi was accused of stealing from clients Girardi was previously married to...

Elon Musk’s introduction to politics

Elon Musk spent the last several months knee deep in government, sidelining his companies to pursue a longstanding Republican quest...

DR Horton, Wells Fargo, Dollar Tree, and More

Key Takeaways U.S. equities had been barely greater at noon as a brand new report on non-public sector hiring missed...

The Hidden Dangers of Earning Risk-Free Passive Income

I’ve been focused on building passive income since 1999, back when I had to be in the office by 5:30...

New Research Suggest Link Between Litigation Funding, Attorney Ads

In accordance with analysis from the American Tort Reform Affiliation (ATRA), authorized service suppliers spent greater than $2.5 billion on...

How to Analyze Market Moves Like a Pro

Key takeaways ChatGPT can simplify and speed up crypto evaluation by decoding market knowledge, summarizing sentiment and producing technique templates....

Semiconductor Supplier GlobalFoundries to Spend $16B to Boost US Chip Production

Key Takeaways GlobalFoundries plans to spend greater than $16 billion to extend chip manufacturing within the U.S. The provider of...

RV Maker Thor Industries Tops Estimates on North America Sales, Cost Controls

Key Takeaways Thor Industries exceeded earnings and income forecasts as North American gross sales elevated and it contained bills. The...

Burning Cargo Ship Carrying 3,000 Vehicles Abandoned Off Alaska

The crew of a cargo ship carrying round 3,000 autos, together with 800 electrical autos, deserted it off the coast...

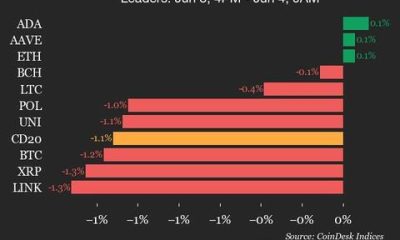

SUI Drops 3.9% as Index Trades Lower from Tuesday

CoinDesk Indices presents its day by day market replace, highlighting the efficiency of leaders and laggards within the CoinDesk 20...

Asana Stock Slumps as Software Maker Warns of Retention Headwinds

Key Takeaways Asana shares dropped 12% in premarket buying and selling Wednesday, a day after the corporate mentioned its web...

5 Things to Know Before the Stock Market Opens

U.S. inventory futures are edging increased as traders digest remarks by President Donald Trump on difficulties negotiating with Chinese language...

Jessie J reveals shocking breast cancer diagnosis in emotional video

Jessie J has been diagnosed with breast cancer. WireImage Jessie J has been diagnosed with early breast cancer. The singer...

As Trump’s Tariffs Nudge Canada Toward Free Interprovincial Trade, Gerard Comeau Gets His Revenge

Gerard Comeau fought again after being fined for bringing an excessive amount of beer into his province. He misplaced the...

Trucordia Gains $1.3B Investment From Carlyle to Propel Growth

Trucordia at the moment introduced it’s going to obtain a $1.3 billion strategic funding from world funding agency Carlyle’s International...

Bitget Partners With University of Zurich Blockchain Center, Providing Opportunities and Scholarships for Students

This content material is supplied by a sponsor. Victoria, Seychelles, June 4 2025 — Bitget, the main cryptocurrency alternate and...

Dollar Tree Tops Q1 Estimates But Expects Profit to Dip Due to Tariffs

Greenback Tree (DLTR) shares fell in premarket buying and selling Wednesday after the low cost retailer warned of a success...

DraftKings Stock Price Levels to Watch After Approval of New Illinois Sports Betting Tax

Key Takeaways DraftKings shares rebounded on Tuesday from a steep decline the earlier session that adopted information Illinois lawmakers had...

Dave’s Hot Chicken Acquired for $1B By Roark Capital

Dave’s Hot Chicken, which began in 2017, announced on Monday that it was acquired by private equity firm (and Subway...

Advanced AI Tool Including Document Analysis and Policy Comparison Tool

Austin, TX — June 04,2025 — The Danger & Insurance coverage Training Alliance is proud to announce the launch of...

One of Africa’s most successful founders is back with a new AI startup and already raised $9M

In 2023, co-founders Karim Jouini and Jihed Othmani bought their expense administration startup Expensya to Swedish procurement software program agency...

This Remote State Has the Most Affordable Health Insurance: See How Yours Stacks Up

This Distant State Has the Most Inexpensive Well being Insurance coverage: See How Yours Stacks Up

The Fed’s Word Of The Day: “Uncertainty”

Key Takeaways Fed officers on Tuesday as soon as once more emphasised their intention to attend and see how President...

Iowa Amusement Park Settles Lawsuit Over 11-Year-Old’s Drowning in 2021

An Iowa amusement park’s former operator has agreed to pay an undisclosed quantity to settle a lawsuit filed by the...

Blockchain can end the food fraud crisis, but it’s a costly battle

Meals fraud siphons as much as $50 billion from the worldwide meals {industry} yearly and endangers public well being. When...

Jessie J Diagnosed with ‘Early’ Breast Cancer

NEED TO KNOW Jessie J revealed that she’s been diagnosed with “early” breast cancer on Tuesday, June 3 According to...

Taylor Swift’s blunt reaction to Blake Lively’s ‘groveling’ revealed

Taylor Swift has reportedly been ghosting Blake Lively after being dragged into the actress’ messy legal battle with Justin Baldoni....

Whitney Purvis Says She’ll ‘Always Cherish’ the Last Hug She Had with Son Weston

NEED TO KNOW Whitney Purvis has shared a new tribute in honor of her son Weston, who died earlier this...

Renée Zellweger hits the red carpet solo as Ant Anstead stays in rich divorcee’s home

She’s solo dolo. Renée Zellweger hit the red carpet alone at the Gotham Television Awards 2025 Monday night after it...

Where Are the ‘Love Island USA’ Winners Now? Here’s Who’s Still Together

Six couples have exited the villa as winners of Love Island USA, but only a few have stayed together. The...

Kristin Cavallari calls cutting father out of her life the ‘best decision’ ever made

Kristin Cavallari has no regrets about cutting off ties from her father, Dennis Cavallari, after he “crossed the boundary” with...

Kylie Jenner Teases Knicks-Colored Lingerie, Worth Nearly $200, for Indianapolis Trip with Timothée Chalamet

NEED TO KNOW Kylie Jenner showed some pricey Knicks-themed lingerie following her appearance at the NBA conference finals with boyfriend...

Phaedra Parks spills ‘RHOA’ tea | Tea Time | Virtual Reali-Tea (Video)

Phaedra Parks spills ‘RHOA’ tea | Tea Time | Virtual Reali-Tea (Video) | Page Six Next Previous

Livvy Dunne’s Death Drop in String Bikini on SI Swimsuit Runway Was ‘Split Decision,’

NEED TO KNOW Livvy Dunne turned heads when she did the splits during Sports Illustrated Swimsuit’s Runway Show 2025 in...

Cardi B makes Stefon Diggs romance Instagram-official

Okurrr. Cardi B made her relationship with NFL star Stefon Diggs Instagram-official days after slamming her ex Offset as a...

Kody Brown Suggests ‘Guy’s Trip’ with Christine’s Husband David

NEED TO KNOW Kody Brown spoke about his ex wife Christine’s new husband, David Woolley, on Sister Wives on Sunday,...

Brian McKnight did not reach out before estranged son Niko’s death: source

Brian McKnight made no effort to reach out to his estranged son Cole “Niko” McKnight before the 32-year-old died from...

‘Race Across the World’ Star Sam Gardiner, 24, Dead After Car Crash

Sam Gardiner, a former Race Across the World contestant, has died following a car crash. He was 24. Gardiner was...

Taylor Swift celebrates regaining masters with bestie Selena Gomez during NYC dinner outing

Girls’ night out. Taylor Swift celebrated regaining the masters to her first six albums by enjoying a lavish dinner outing...

Lady Gaga Joining ‘Wednesday’ Season 2 as Netflix Drops First 6 Minutes

NEED TO KNOW Netflix unveiled the first six minutes of Wednesday‘s highly anticipated second season at its Tudum 2025 live...

Timothée Chalamet’s ex makes surprising comments about Kylie Jenner romance

No bad blood here. Eiza González took the high road when asked about her ex Timothée Chalamet’s new romance with...

Kate Hudson Says Mindy Kaling Sent ‘Running Point’ Notes Right After Giving Birth

NEED TO KNOW Kate Hudson said Mindy Kaling, 45, was sending script notes about their show Running Point “like an...

The summer 2025 fashion trends worth shopping, according to a celebrity stylist

Page Six may be compensated and/or receive an affiliate commission if you click or buy through our links. Featured pricing...

Melissa McCarthy Shares Rare Photo of Her Daughter as She Goes to Prom

NEED TO KNOW Melissa McCarthy shared a photograph of her daughter, Vivian Falcone, 18, on her Instagram Stories on Friday,...

‘RuPaul’s Drag Race’ All Stars 10 Ep. 5 recap ft. Kerri Colby

“Everyone knows you don’t trust a fat, nasty bitch!” Mistress Isabelle Brooks had no regrets after outwitting the competition on...

Selena Gomez Congratulates Taylor Swift on Reclaiming Her Music Catalog

NEED TO KNOW Selena Gomez shows support for Taylor Swift regaining control of her masters The “Cruel Summer” singer’s music...

Cardi B reveals her and estranged husband Offset’s third baby’s name

Cardi B revealed her and Offset’s third baby’s name. Instagram/@iamcardib Cardi B revealed the name of her and Offset’s third...

Jamie Lee Curtis Marks 3 Years Since Hosting Daughter Ruby’s Cosplay Wedding

NEED TO KNOW Jamie Lee Curtis shared a tribute post honoring her daughter Ruby’s backyard wedding with a throwback photo...

Bethenny Frankel, 54, turns up the heat in tiny bikini

Bethenny Frankel is ready for Miami Swim Week! The “Real Housewives of New York” alum, 54, took to Instagram Thursday...

Gigi and Bella Hadid Introduce Their 23-Year-Old Half-Sister Aydan Nix

NEED TO KNOW Gigi and Bella Hadid announced on Thursday, May 29, that they have another sister The supermodels revealed...

Audra McDonald hits back at Broadway rival Patti LuPone’s diss

Audra McDonald gracefully clapped back after Patti LuPone claimed they weren’t friends. “If there’s a rift between us, I don’t...

Kate Winslet Covered Daughter Mia Threapleton’s Eyes During ‘Titanic’ Sex Scene

NEED TO KNOW Kate Winslet’s daughter Mia Threapleton revealed that she has never actually seen the entirety of Titanic in...

Kylie Jenner reveals why she wore black gowns at awards shows with Timothée Chalamet

Never underestimate the power of a LBD. Kylie Jenner revealed why she stuck to the timeless, always-in-style look this awards...

Happy Birthday, Zaya Wade! Celebrate with Her 13 Most Stylish Moments Yet (PHOTOS)

Zaya Wade is one stylish teenager! The model, who turns 18 on May 29, 2025, might have made her runway...

Justin Bieber shares handsy photos with Hailey to celebrate $1B Rhode deal

Looks like Justin Bieber can’t keep his hands to himself. The “Peaches” singer shared PDA-packed photos with wife Hailey Bieber...

How Trump’s Pardon Impacts Chrisley Family’s New Reality Show (Source)

NEED TO KNOW The Chrisley family is gearing up to launch an all-new reality series at Lifetime, but a source...

Barbara Walters doc revisits savage interviews with Taylor Swift, Trump, the Kardashians and more

A new Hulu documentary is revisiting Barbara Walters’ most scathing interviews throughout her decades-long career. In a sneak peek trailer...

Soap Star Paul Danan Found Dead on Sofa in Front of TV, Says Coroner

NEED TO KNOW Paul Danan was found dead sitting on his sofa after taking a lethal cocktail of drugs at...

‘Speechless’ Savannah Chrisley reveals next steps for Todd and Julie after Trump’s pardons

Savannah Chrisley tearfully revealed she’s preparing for her parents, Todd and Julie Chrisley, to return home after President Trump pardoned...

Chase Chrisley Speaks Out After Trump Pardons Parents Todd and Julie

NEED TO KNOW Chase Chrisley expressed gratitude for President Donald Trump after he granted Todd and Julie Chrisley pardons on...

-

Life Style3 weeks ago

Life Style3 weeks agoPositive and Funny Sayings for Your Best Friend and Family

-

Life Style2 weeks ago

Life Style2 weeks ago2 Small Ways to Start Living the Life You Truly Want

-

Technology2 weeks ago

Technology2 weeks agoHeybike’s Alpha step-through e-bike is an affordable, all-terrain dreamboat

-

Entertainment3 weeks ago

Entertainment3 weeks agoStorm Reid Celebrates Her USC Graduation

-

Technology2 weeks ago

Technology2 weeks agoAlt Carbon scores $12M seed to scale carbon removal in India

-

Life Style3 weeks ago

Life Style3 weeks ago91 Funny Birthday Quotes for Friends with Hilarious Humor That Will Make You Laugh

-

Technology3 weeks ago

Technology3 weeks agoThousands of people have embarked on a virtual road trip via Google Street View

-

Entertainment3 weeks ago

Entertainment3 weeks agoEverything We Know About the Husbands and Partners of The Secret Lives of Mormon Wives Cast