Finance & Banking

Here’s How Much Elder Caregivers Charge in 2026—Is Your Family Paying Fair Rates?

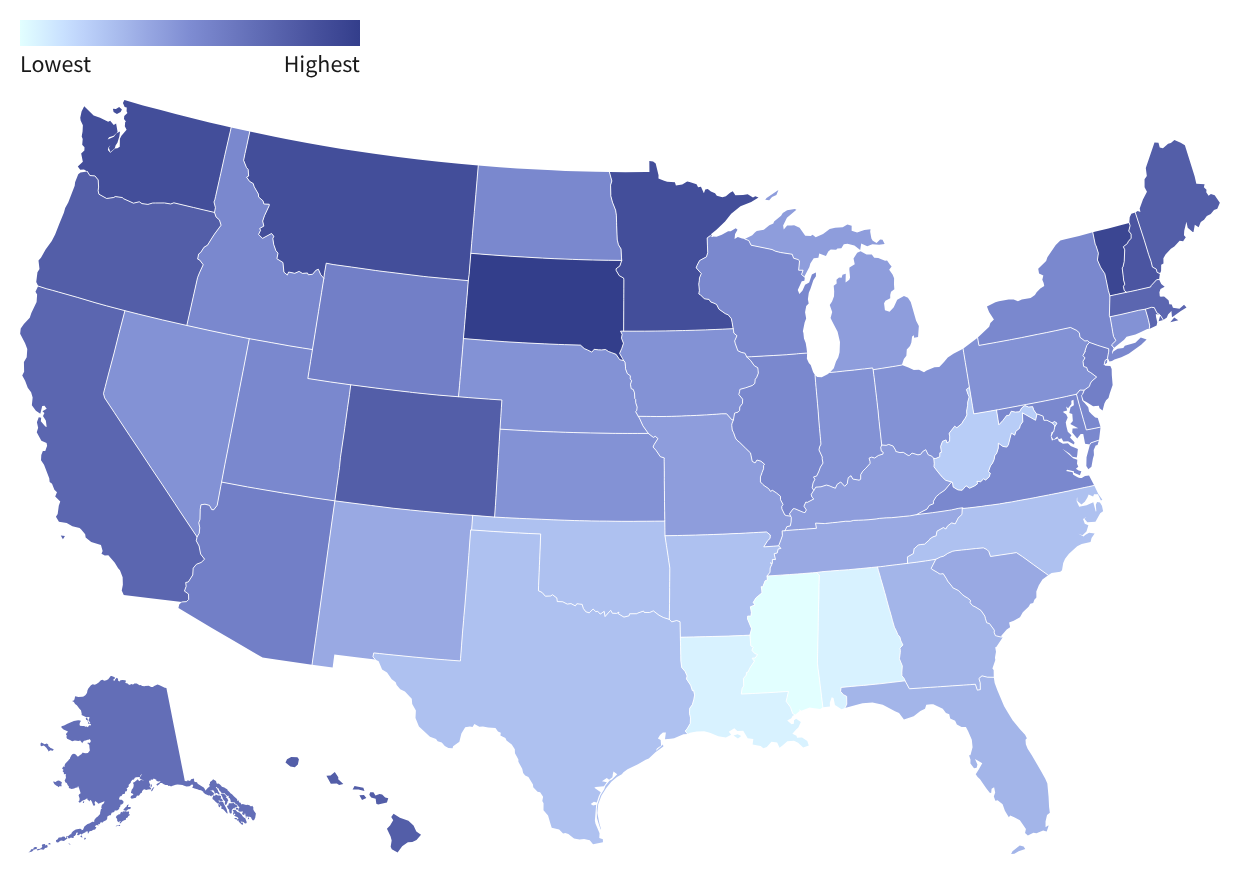

:max_bytes(150000):strip_icc():format(jpeg)/taTza-what-older-adult-care-costs-in-every-state-1-b59868b9cb884e49be9ee9422abdf24f.png)

Key Takeaways

- Home care rates vary from $25 per hour in Mississippi to $44 per hour in South Dakota—geography, not care quality, drives the biggest price differences.

- Nearly one-third of families end up paying more than they expected for care, often because they started researching costs after a health crisis forced their hand.

Get personalized, AI-powered answers built on 27+ years of trusted expertise.

If you’re hiring a home caregiver for a loved one in 2026, what state you live in may determine a lot about how much you’ll pay.

Families paid a median of $34 an hour for a home caregiver in the U.S. last year, according to an annual report by A Place for Mom, an assisted care and senior living comparison site. That’s up 3% from a year ago.

Many families assume Medicare will cover long-term senior living—in general, it doesn’t. According to Tatyana Zlotsky, CEO of A Place for Mom, “that realization often comes at the worst possible moment: during a health event, a hospital discharge, or a sudden decline.” Zlotsky added that families often “don’t accurately estimate or understand the costs of each type of care and what they include.”

A Coast-to-Coast Price Check on Home Care

The national median masks enormous state-by-state swings. Mississippi families pay $25 an hour for home care. In South Dakota, the same service costs $44.

High-cost states like California and New York don’t even crack the top five. Instead, the priciest states include South Dakota, Vermont, Montana, Minnesota, and Washington—places where thin labor pools and rural geography push caregiver wages higher.

On the affordable end, the South dominates. Alabama and Louisiana both sit at $26 per hour, while Mississippi, West Virginia and Arkansas round out the bottom five.

Fast Fact

More than 10,000 Americans turn 65 every day, and roughly 70% of people who reach that age will need some form of long-term care. Medicare doesn’t cover most home care services, leaving families to shoulder costs that financial advisors say too few people plan for.

More Demand, Fewer Workers, Higher Bills

Three forces are pushing up the pricing of at-home care.

Workforce shortages keep pushing caregiver wages up; there aren’t enough workers to meet demand from a rapidly aging population. Inflation has raised operating expenses—food, insurance, transportation—that agencies pass along to families. And post-pandemic demand has tightened the market, giving agencies less reason to compete on price.

The 3% year-over-year jump in home care costs outpaced the broader consumer price index. And home care isn’t the only category climbing. Assisted living rose 4.4% to $5,419 a month; memory care jumped 3.7% to $6,690 a month.

For families weighing home care versus these kinds of facilities, Zlotsky noted “there is a threshold when full-time home care can be more expensive than senior living, especially in some of the lower-cost states.”

Stop Guessing, Start Comparing

The biggest risk isn’t a high hourly rate but not knowing the rate until an emergency hits. Only 18% of people say they understand care costs well, according to A Place for Mom data. About one-third reported they paid more than they expected after a move.

“What surprises many families is that the monthly rate you see advertised is just the starting point,” Zlotsky said. As care needs increase, additional services can raise costs faster than expected.

Lily Vittayarukskul, founder of long-term care planning platform Water Lily, built her company after watching her own family navigate a relative’s terminal illness without a plan.

“I saw intimately firsthand a lot of the core devastating effects of not talking about the topic ahead of time, on both your finances, your family, your familial relationships, but honestly, your quality of life that you get by not doing the planning,” she said.

Start planning by benchmarking your state. If you’re in a state where the median sits near or above $40 per hour, build your budget at the higher end. If you’re in the South or Midwest, rates in the mid-$20s to low-$30s are typical, but limited supply in some rural markets can still push costs above the median.

Compare several agencies before signing. Hourly rates reflect starting prices, but actual costs vary by the type of care (companion care vs. skilled nursing), hours per week, and whether you need overnight or weekend coverage. Ask about rate increases, too: with costs climbing 3% annually, your starting rate won’t be your rate a year from now.

“Start the conversation before a crisis forces it,” Zlotsky said. “Even one honest conversation this week can make a meaningful difference later.”

Finance & Banking

Major Indexes Plunge Amid Tariff Uncertainty; Dow Sheds 800 Points; Bitcoin Drops, Safe-Haven Gold Rises

:max_bytes(150000):strip_icc():format(jpeg)/GettyImages-2260936030-f67bccf383fa46b38e6df63b54a60ff9.jpg)

February 23, 2026 12:53 PM EST

Netflix Stock Drops as Trump Sets Sights on Director Susan Rice

FROM 5 minutes ago

The President didn’t exactly weigh in on the Netflix-Warner Bros. Discovery deal over the weekend. But it looked enough like he did that he’s moving markets today.

Shares of Netflix (NFLX) were recently dropping following a statement on Truth Social that said the streaming video giant “should fire” Susan Rice, a member of its board of directors who also served the past three Democratic presidents. President Donald Trump’s Saturday post did not specifically mention Netflix’s planned acquisition of Warner Bros. (WBD), but it responded to another person’s post, which advocated against it.

Thomas Fuller / NurPhoto via Getty Images)

That seemed to inflame investor concern that the Netflix-Warner Bros. deal, its future already uncertain after negotiations with competing Warner suitor Paramount Skydance (PSKY) were reopened last week—might face challenging regulatory obstacles.

The White House did not provide an additional statement to Investopedia in time for publication, and Netflix didn’t respond to a request for comment. Rice could not be reached in time for publication. An updated bid from Paramount Skydance is expected sometime today.

Read the full article here.

February 23, 2026 11:30 AM EST

Novo Nordisk Stock Tumbles Monday to Its Lowest Point in Nearly 5 Years. Here’s Why

FROM 1 hr 28 min ago

The weight-loss drug wars took a fresh turn on Monday.

Shares of Novo Nordisk (NVO) were down over 15% in recent trading after the Danish drugmaker announced the results of a clinical trial for its new weight-loss drug that came in short of expectations.

Kristian Tuxen Ladegaard Berg / NurPhoto / Getty Images

Novo Nordisk said that among a group of 809 people, the average weight loss for a patient taking its in-development drug CagriSema was about 23% of a patient’s body weight after 84 weeks. That was lower than the 25.5% mark for those in the trial that took tirzepatide, the active ingredient in Eli Lilly’s (LLY) Mounjaro and Zepbound.

The result marks the latest CagriSema trial to drag on sentiment surrounding the Ozempic and Wegovy maker’s stock amid growing worries about competition from rival Eli Lilly.

Read the full article here.

February 23, 2026 11:05 AM EST

Arcellx Stock Skyrockets as Biotech Acquired by Gilead Sciences

FROM 1 hr 54 min ago

Monday has been an awful day for equities investors thus far. Not so for Arcellx shareholders.

Arcellx (ACLX) stock skyrocketed 77% after the biotech firm entered into an agreement to be acquired by Gilead Sciences (GILD) for $115 per share in cash and one contingent value right of $5 per share, or $7.8 billion.

Arcellx shares, which closed at $64.11 each Friday, were trading around $114 recently. They had been little changed over the past 12 months until today.

Arcellx and Kite, a Gilead company, already were collaborating to co-develop and co-commercialize Arcellx’s anitocabtagene autoleucel (anito-cel), which treats patients with multiple myeloma.

“This agreement reflects our conviction in the potential of anito-cel and our intention to move with speed so we can make the most of that potential for patients with multiple myeloma,” Gilead CEO Daniel O’Day said. “Beyond the potential launch this year, anito-cel could become a foundational treatment for multiple myeloma over time, including earlier lines of therapy.”

The companies anticipate the deal will close in the second quarter.

TradingView

February 23, 2026 08:59 AM EST

Blizzard Cancels Thousands of Flights Across East Coast

FROM 3 hr 59 min ago

The snowstorm currently working its way across the East Coast is wreaking havoc on air travel, with over 5,300 flights cancelled in the U.S. already for Monday alone, per the flight tracking website FlightAware.

There were more than 7,500 delays and 3,400 cancellations on Sunday as the storm started to batter the coast.

Michael Nagle /Bloomberg via Getty Image s

Cancellation rates are near or above 90% at several airports including New York’s John F. Kennedy International and LaGuardia, and Boston Logan International, among others.

Shares of major airlines were lower before the bell, with United Airlines (UAL) and American Airlines (AAL) each down about 1%, while Delta Air Lines (DAL) slipped 0.5%.

February 23, 2026 08:22 AM EST

Domino’s Pizza Stock Surges on Revenue, Same-Store Sales Beat

FROM 4 hr 36 min ago

Domino’s Pizza CEO Russell Weiner says the company’s “Hungry for MORE” strategy is paying off.

Shares of Domino’s (DPZ) surged 6% before the bell Monday after the Ann Arbor, Mich.-based pizza giant reported better-than-expected revenue and same-store sales.

Domino’s posted fiscal 2025 fourth-quarter revenue of $1.54 billion, up 6.4% year-over-year and topping the consensus $1.52 billion estimate of analysts surveyed by Visible Alpha.

Same-store sales growth of 3.7% easily topped expectations of 2.0%, although earnings per share of $5.35 came up just short of estimates.

Mike Kemp / In Pictures via Getty Images

“In 2025 we demonstrated that when we execute our Hungry for MORE strategy it delivers MORE sales, MORE stores, and MORE profits,” Weiner said, referring to the company’s five-year plan to “grow and win as a brand.”

Domino’s board approved a 15% quarterly dividend increase to $1.99 per share, to be paid on March 30 to shareholders of record as of March 13.

Domino’s shares entered Monday down nearly 8% this year and 17% over the past 12 months.

February 23, 2026 07:29 AM EST

Home Depot and Lowe’s Report Earnings This Week. Here’s How Much the Stocks Are Expected to Move

FROM 5 hr 30 min ago

Home Depot and Lowe’s are set to report earnings this week, with traders anticipating sizable swings in the home improvement retailers’ stocks following the results.12

Home Depot is set to report earnings on Tuesday morning, with rival Lowe’s following Wednesday. Current options pricing suggests traders expect Home Depot (HD) stock could move up to 4% in either direction by the end of the week, while Lowe’s (LOW) could swing up to 5%.

Yuki Iwamura / Bloomberg / Getty Images, PATRICK T. FALLON / Contributor / Getty Images

For Home Depot, a shift of that size from Friday’s close could lift the stock above $398, its highest level since last September, or drag the stock down to $366. For Lowe’s, the move could mean setting a record high above $294 at the high end, or dropping as low as $266.

Both stocks have enjoyed a strong start to the year so far, with Home Depot gaining about 11% and Lowe’s up 16% for 2026, amid a broader rotation out of tech stocks in favor of consumer-focused companies.

Read the full article here.

February 23, 2026 06:53 AM EST

Stock Futures Fall Amid Tariffs Uncertainty

FROM 6 hr 5 min ago

Futures contracts connected to the Dow Jones Industrial Average pointed 0.3% lower.

TradingView

S&P 500 futures also were down 0.3%.

TradingView

Nasdaq 100 futures declined 0.5%.

TradingView

Finance & Banking

How Much Are Americans Saving? A Look at Bank Balances

:max_bytes(150000):strip_icc():format(jpeg)/GettyImages-2086436224-4b76a2e22e8c42c7bfaf05823e77b0f6.jpg)

Key Takeaways

- Median bank account balances in the U.S. range from $5,400 for those under 35 to $13,400 for ages 65–74, according to Federal Reserve data.

- Couples report higher median savings than single households.

- College-educated households have the highest bank balances.

- The data reflects median—not average—savings, offering a more accurate snapshot of what typical Americans hold in their bank accounts.

- To boost your savings faster, consider a top high-yield savings account, money market account, or CD.

How Much Cash Americans Keep in the Bank—And Where You Stand

Ever wondered how your bank balance compares to others? Federal Reserve data reveals what savings a typical American has by age, household type, and education.

According to the Fed’s Survey of Consumer Finances, the median amount held in bank accounts across all American households in 2022 (the most recent data available) was $8,000. This amount is in transaction accounts, which include checking, savings, money market, and brokerage cash accounts, as well as prepaid debit cards. (Certificates of deposit and retirement accounts are not part of this grouping.)

But that $8,000 figure only tells part of the story. Median balances vary widely by age, household type, and education.

Important

We use median figures instead of averages to avoid skewed results from people with very high or very low savings. The median represents the middle point—half of respondents have more savings, and half have less.

Bank Balances by Age: How Do You Compare?

The Federal Reserve looks at multiple age groups in its survey:

- Under 35

- 35-44

- 45-54

- 55-64

- 65-74

- 75 or older

In the most recent survey (2022), more than 98% of Americans across every age group reported having money in bank accounts. But median balances varied sharply by age. For instance, those under 35 had a median of $5,400, while Americans 75 and older held a median of $10,000.

Bank Balances by Household Type: Where Do You Fall?

In its survey, the Fed uses five breakdowns for family structure:

- Single With Child(ren)

- Single, No Child, Age <55

- Single, No Child, Age >=55

- Couple With Child(ren)

- Couple, No Child

Bank account median values varied widely between singles and couples. In 2022, single adults over 55 with no children had the highest median balance among individuals ($4,300). For couples, those without children held the highest median balance ($16,000).

Bank Balances by Education Level: How Do You Stack Up?

The Fed survey includes four options for education level:

- No High School Diploma

- High School Diploma

- Some College

- College Degree

Survey results suggest a strong link between educational level and median bank balances, much more than age or family structure. High school graduates reported median savings more than three times higher than those without a diploma. College graduates had over four times the median balance of those with some college education but no degree.

Want a Bigger Bank Balance? Open a High-Yield Account

However much cash you have in the bank, it’s smart to make sure it’s earning more for you. Putting some money into a high-yield savings account, money market account, or certificate of deposit (CD) can help boost your savings balances.

A high-yield savings account is among the easiest places to deposit your money, giving you access to your cash anytime you need it. Because the annual percentage yield (APY) from different banks varies widely, look for one that works for you. Our list of the best high-yield savings accounts includes several options that pay at least 4.02% APY, with the best rate being 5.00% APY. Just be aware that rates on savings accounts are variable, meaning the bank can change your APY at any time without warning.

Money market accounts are similar to savings accounts and offer check-writing abilities. If that’s an important feature for you, you can check out the best money market accounts—and several currently offer APYs of 3.20% or better, with a top rate of 4.00% APY. But as with savings accounts, money market APYs can change.

If you don’t need to access your money immediately, a certificate of deposit (CD) is a safe option with a big perk: a fixed rate that you can lock in for months or years. Your bank or credit union will guarantee a set APY for terms generally ranging from 3 months to 5 years in exchange for you keeping your money in the CD. You’re able to determine now how much money you’ll earn when the CD matures, and some of the best CD rates—now up to 4.50% APY—are good into 2026 or beyond, regardless of what happens to interest rates in the short term. Just be sure to pick your term carefully, as you’ll be hit with an early withdrawal penalty if you cash out before the maturity date.

Finance & Banking

Retiring Next Year? Discover the Right Monthly Income Target

:max_bytes(150000):strip_icc():format(jpeg)/GettyImages-1386208288-245b88700837486bafd0511175200f57.jpg)

Key Takeaways

- Financial experts say you’ll need about 70% to 80% of your pre-retirement income to maintain your lifestyle in retirement.

- For the median U.S. household income ($83,730), you’d need about $5,233 per month in retirement.

- Using the 4% rule, that means that you’d need to save $1.57 million in total.

Get personalized, AI-powered answers built on 27+ years of trusted expertise.

When preparing for retirement, you’re probably wondering, will I have enough? To answer this, you’ll need to know a few key numbers. First, how much money will you need per month in retirement? And then, how much money will you need to save in total? Read on to learn how to crunch these numbers and get the answers you’re looking for.

How Much Do You Need per Month in Retirement?

First, we need to calculate how much money you’ll need per month in retirement.

If you want to continue the lifestyle you’re living now, just multiply your current income by 75%.

That’s because your costs in retirement will likely be about 70% to 80% of the costs you have now.

So if you currently make the median income in the U.S. per year ($83,730), plan on spending around $62,800 per year, or around $5,230 per month, in retirement.

How Much Do You Need to Save for Retirement?

Now that we know how much you’ll need per year and per month in retirement, we can calculate how much you’ll need to save in total.

There’s a rule of thumb called the 4% rule. It says that for a 30-year retirement, you can safely withdraw 4% of your retirement savings per year, adjusted for inflation each year.

Let’s use the numbers we used above. Someone with the median income in the U.S. ($83,730) can plan on spending around $62,800 per year in retirement. Using the 4% rule, we divide $62,800 by 4%, resulting in about $1.57 million. That’s how much you’ll need to save in total.

Important

Recent studies suggest that with current rates of inflation, retirees should actually limit their withdrawals to 3.7%.

If we use 3.7% instead of 4%, we divide $62,800 by 3.7%, resulting in about $1.7 million. That’s a more conservative estimate of how much you’ll need to save in total.

Factors that Influence Your Spending in Retirement

Your income needs may fluctuate as you move through retirement. You might spend more in early retirement because you’ll be relatively active and enjoying your new lifestyle. At some point, though, you might settle down. During this middle stage of retirement, your spending might decrease. In late retirement, your spending might increase as you face various medical bills and the cost of care.

Your spending will also depend on your location and lifestyle. For instance, if you dream of traveling in retirement, you’ll likely spend more than others who prefer to stay close to home. Retirees who live in certain areas will likely pay more for housing and care, which means they’ll need more income in retirement than someone who lives in a more affordable area.

The Bottom Line

Planning for retirement takes a little math. First, assume that you’ll spend about three-quarters (75%) of your current monthly income in retirement. Then use the 4% rule to discover how much you’ll need to save for retirement in total. Tweak the formula to suit your needs and consider your retirement goals, as well as the cost of living in your area. The more prepared you are, the more you can sit back and enjoy your retirement.

Here’s How Much Elder Caregivers Charge in 2026—Is Your Family Paying Fair Rates?

Key Takeaways Home care rates vary from $25 per hour in Mississippi to $44 per hour in South Dakota—geography, not...

Utah Jazz rookie Ace Bailey is developing at his own pace this season

On one of the first road trips of his young NBA career, the 6-foot-9 future of the Utah Jazz climbed...

Ioan Gruffudd claims ex-wife Alice Evans threatened to ‘Amber Heard’ him as dramatic trial kicks off

Ioan Gruffudd testified that his ex-wife, Alice Evans, threatened to destroy his career by making false, explosive accusations against him....

Making frontier cybersecurity capabilities available to defenders \ Anthropic

Claude Code Security, a new capability built into Claude Code on the web, is now available in a limited research...

Major Indexes Plunge Amid Tariff Uncertainty; Dow Sheds 800 Points; Bitcoin Drops, Safe-Haven Gold Rises

February 23, 2026 12:53 PM EST Netflix Stock Drops as Trump Sets Sights on Director Susan Rice FROM 5 minutes...

Kylie Jenner looks visibly uncomfortable at Alan Cumming’s cheeky joke at BAFTAs

Kylie Jenner was visibly uncomfortable when host Alan Cumming made a rather cheeky joke at the 2026 BAFTAs Sunday. During...

2-6 inches of snow expected in DC area; school delays possible – NBC4 Washington

After starting out as rain, clumpy wet snowflakes began falling Sunday afternoon in the D.C. area. While it’s not sticking...

How Much Are Americans Saving? A Look at Bank Balances

Key Takeaways Median bank account balances in the U.S. range from $5,400 for those under 35 to $13,400 for ages...

Clippers Notes: Lopez, Leonard, Collins, Garland

Brook Lopez joined the Clippers to serve as a veteran backup to Ivica Zubac, but now it looks like he’ll...

Jennifer Lopez celebrates twins Emme and Max’s 18th birthday with sweet tribute

Jennifer Lopez shared an emotional tribute to her twins, Max and Emme, on their 18th birthday. The singer and actress...

Retiring Next Year? Discover the Right Monthly Income Target

Key Takeaways Financial experts say you’ll need about 70% to 80% of your pre-retirement income to maintain your lifestyle in...

Final Injury Report for Raptors-Bucks: Will Scottie Barnes, Giannis Antetokounmpo Play?

The Toronto Raptors are on the road on Sunday afternoon as they travel to take on the Milwaukee Bucks in...

Tim McGraw reveals most controversial song Indian Outlaw after industry tried to cancel hit

Tim McGraw is looking back at the most “controversial” song of his career. During a recent interview on “The Tim Ferriss...

Earnings From Nvidia, Home Depot, Banks, and Berkshire; Trump Speech

Earnings from Nvidia, the world’s most valuable company, and President Donald Trump’s State of the Union address take center stage...

Momentos históricos de tormentas de nieve en Nueva York – Telemundo New York (47)

Los restos de la última gran tormenta de nieve de hace casi un mes aún se adhieren a las aceras...

How to Rent a Car in South Africa Without a Credit Card: Real Options Explained

Many travelers want flexible and simple car rental options in South Africa. Credit cards are not always convenient for every...

Is OctaFX Legit? Examining the Broker’s Global Standing

The world of modern finance has become one of the most dynamic and fast-growing environments. Today, technology, investment, and online...

Smarter Maintenance Management: How Digital Tools Are Transforming Preventive Maintenance and Facility Operations

In every modern industry — from manufacturing plants to amusement parks — equipment reliability defines performance. Unexpected downtime, inefficient scheduling,...

CisporaSeek: The Smarter Way to Search and Discover Information

We live in a time where there’s no shortage of information — but finding the right information can still feel...

Timur Turlov – Empowering Global Finance Through Innovation and Vision

In the world of modern finance, few entrepreneurs have captured global attention like Timur Turlov. As the founder and CEO...

Oprah’s Roomy Cargo Pants Are a Go-To Fall Style

Welcome to The Blueprint, where we break down the celebrity looks we want to wear right now and build them...

AI the New Tech Stack

The Internet Computer ICP$4.7751, a blockchain project that has sought to differentiate itself from rivals, is doubling down on its...

How A Irrevocable Life Insurance Trust Can Reduce Estate Taxes

Lately, I’ve been thinking more about estate planning. Part of it is just getting older. Part of it is having...

Karlie Kloss welcomes third baby with husband Joshua Kushner

Karlie Kloss’ brood just got bigger. The model has given birth to her and husband Joshua Kushner’s third baby —...

Even Time-Strapped Business Owners Can Share an Engaging Reading Experience with Their Kids

Disclosure: Our goal is to feature products and services that we think you’ll find interesting and useful. If you purchase...

Russian Finance Minister: Ruble Is “Strong,” Enhances Budget Traceability

Anton Siluanov, Russia’s finance minister, said the digital ruble, Russia’s CBDC, is a “strong” and “reliable” alternative to the fiat...

The End Of The Commercial Real Estate Recession Is Finally Here

Since 2022, commercial real estate (CRE) investors have been slogging through a rough downturn. Mortgage rates spiked as inflation ripped...

Prince Harry Made Secret Visit to Another Member of Royal Family During U.K. Trip

NEED TO KNOW Prince Harry’s four-day visit to the U.K. included a secret visit to another member of the royal...

White House offers more details about potential TikTok deal

White House Press Secretary Karoline Leavitt appeared on Fox News today and said that an agreement has been reached —...

Matthew McConaughey reveals the bedroom secret that helped his marriage

Bigger isn’t always better. Matthew McConaughey revealed in his new book that downsizing his bed helped him get closer to...

Flora Growth Launches $401M Treasury to Back 0G AI Blockchain

Nasdaq-listed cannabis firm Flora Growth has launched a $401 million treasury initiative to back Zero Gravity (0G), a blockchain project...

This Is a Rare Chance to Save More Than 70% on QuickBooks Desktop Pro Plus 2024

Disclosure: Our goal is to feature products and services that we think you’ll find interesting and useful. If you purchase...

Jordin Sparks Reveals If Son DJ, 7, Wants to Become a Singer

NEED TO KNOW Jordin Sparks attended the Elizabeth Taylor Night of Compassion at the Beverly Hills Hotel in California on...

The Upside of Grindcore Culture: Work Hard, Profit Harder

The grindcore culture is back and grindier than ever. At least that’s what Are Kharazian, an economist at fintech startup Ramp,...

Kalshi Outpaces Polymarket in Prediction Market Volume Amid Surge in U.S. Trading

Kalshi is pulling ahead in the prediction market race, capturing a dominant share of trading volume even as competitors like...

Police kill carjacking suspect outside In-N-Out Burger in Laguna Hills

A man suspected of fatally shooting a woman outside an apartment complex in Carlsbad and stealing her SUV late Friday...

Nepal Uprising Is Latest Challenge to India’s Backyard Diplomacy

The overthrow of Nepal’s government is the latest in a series of uprisings among India’s neighbors, creating a political churn...

D4vd concert dates canceled as police investigate death of 15-year-old girl found in singer’s Tesla

The remaining dates for the d4vd Withered 2025 World Tour appear to have been canceled, as a Los Angeles police...

Fireworks show co-organized by Arc’teryx and artist Cai Guoqiang in Xizang’s Himalayas draws backlash over ecology and cultural disrespect

Cai Guoqiang stages a fireworks display in the Himalayas of Southwest China’s Xizang Autonomous Region on September 20, 2025. Photo:...

Microbial Life Colonizes Post-Impact Craters And Thrives For Millions Of Years

78 million years ago, a 1.6 km asteroid slammed into what is now Finland, creating a crater 23 km (14...

Swiatek sweeps Saturday doubleheader; to face Alexandrova in Korea Open final

A rainout the previous day created a packed Saturday schedule at the Korea Open, with both the quarterfinals and semifinals...

‘We’re not North Korea.’ Newsom signs bills to limit immigration raids at schools and unmask federal agents

In response to the Trump administration’s aggressive immigration raids that have roiled Southern California, Gov. Gavin Newsom on Saturday signed...

I Look at This Country and I See a Stranger

This is one of those moments in history.

Why Hiring an Auto Accident Attorney in Charlotte, NC Can Improve Your Case

Life after a car accident can be overwhelming. Between medical care, car repairs, and figuring out what comes next, it...

Sacramento ABC TV station building struck by gunfire, police say

A man has been arrested in connection with a shooting at a television station building in Sacramento faces a federal...

Thousands protest in Philippines over flood-control corruption scandal

MANILA, Philippines (AP) — Thousands of protesters took to the streets in the Philippine capital on Sunday to express their...

Will We Ever Make it to Mars?

You know, if you take away the lack of air and water, the weaker Sun, the lower gravity, and the...

LAPD searching for suspect after stabbing on Metro bus in South L.A.

Los Angeles police are searching for a man suspected of stabbing and wounding another man during a confrontation aboard a...

Ellen DeGeneres says she was ‘kicked out of show business.’ Is it time to welcome her back?

Ellen DeGeneres People in entertainment LGBTQ issues TV shows See all topics Facebook Tweet Email Link The Cotswolds, England — ...

New video out from stage version of Prince’s ‘Purple Rain’

Rehearsals for the stage adaptation of Prince’s “Purple Rain” are in full swing and the lead performers have been experimenting...

They Helped Oust a Dictator. Now the New Regime Is Coming for Them.

President Daniel Ortega of Nicaragua and his wife, who is co-president, have been arresting longtime loyalists, in an apparent quest...

How Justin Timberlake and Jessica Biel Are Navigating ‘New Normal’

Jessica Biel has been by husband Justin Timberlake’s side amid his battle with Lyme disease. “Jessica has been extremely supportive...

Where to watch South Carolina-Missouri game: time, SEC schedule

US LBM Coaches Poll: Georgia looks strong, Clemson drops out USA TODAY Sports’ Paul Myerberg breaks down Georgia’s comeback win...

Canes Set for Showdown Against Rival Gators

Beck, of course, isn’t the only Hurricane eager to get on the field and face the Gators (1-2). Defensive lineman...

National Cheeseburger Day 2025 deals at McDonald’s, Burger King, more

How to eat burgers without making a mess Keep your hands clean and your burger intact with this simple wrapping...

College football Week 4 preview – DJ Lagway, Arch Manning try to get right

Bill ConnellySep 19, 2025, 07:00 AM ET Close Bill Connelly is a writer for ESPN. He covers college football, soccer...

Riot Fest Returns To Chicago This Weekend. Here’s What You Need To Know

DOUGLASS PARK — Riot Fest is back in Douglass Park this weekend for its 20th anniversary with Blink-182, Weezer and...

Disney faces legal battle with Morgan & Morgan over Steamboat Willie

ORLANDO, Fla. (AP) — Is Steamboat Willie “For the people?” That’s a question that one of the largest personal injury...

Seminole County deputies shoot and kill child porn suspect

LONGWOOD, Fla. — Seminole County Sheriff Dennis Lemma says his deputies shot and killed a child porn suspect. What You...

Access Denied

Access Denied You don’t have permission to access “http://www.espncricinfo.com/series/men-s-t20-asia-cup-2025-1496919/afghanistan-vs-sri-lanka-11th-match-group-b-1496930/ball-by-ball-commentary” on this server. Reference #18.4b5d1502.1758204766.23ff82f https://errors.edgesuite.net/18.4b5d1502.1758204766.23ff82f Source link

Garden City Based Car Crash Injury Lawyer at Bull Attorneys Now Expanding Legal Services to Topeka and Kansas City KS

Bull Attorneys, P.A. Expanding Legal Representation for Car Accident Victims Across Kansas Wichita, Kansas, Sept. 16, 2025 (GLOBE NEWSWIRE) —...

West Nile virus death: Person dies related to mosquito bite in suburban Cook County, officials say

ByABC7 Chicago Digital Team Wednesday, September 17, 2025 5:01PM The Cook County Department of Public Health said this was the...

USA knock Cuba out of Men’s Volleyball World Championship

Robinson emerged as the best scorer of the match with 14 points. He spiked 13 points at a 59% success...

Gen V review – the male full-frontal really is gratuitous | Television

Two years after we last joined its troubled teens in their battle against the forces of corporate tyranny, superhero drama...

Red Sox vs. Athletics lineups and preview for September 16

The Athletics will again counter with Jeffrey Springs, who allowed five runs on eight hits en route to taking the...

Death on the Riviera: The White Lotus is coming to France | The White Lotus

The White Lotus didn’t have the Emmys it expected this year, but a little thing like critical disappointment isn’t going...

Silent Hill f Review Embargo Lifts A Few Days Ahead Of Release

1 Details regarding the review embargo for Konami and NeoBards Entertainment‘s upcoming survival horror game, Silent Hill f, have been...

2025 NFL Week 2 betting – Monday Night Football: Buccaneers-Texans and Chargers-Raiders

Sep 15, 2025, 09:55 AM ET The NFL’s Week 2 slate wraps up with a “Monday Night Football” doubleheader. The...

Trump administration launches pilot program for air taxis : NPR

An electric vertical takeoff and landing (eVTOL) aircraft, flies above the Joby eVTOL aircraft, during a demonstration of eVTOLs Nov....

Redox-driven mineral and organic associations in Jezero Crater, Mars

Farley, K. A. et al. Mars 2020 mission overview. Space Sci. Rev. https://doi.org/10.1007/s11214-020-00762-y (2020). Farley, K. A. et al. Aqueously...

Football Improves to 3-0 With Win Over Langston

RIO GRANDE VALLEY – The University of Texas Rio Grande Valley (UTRGV) Vaqueros football team won their...

Marlon Wayans ‘lost 20 lbs’ for ‘Scary Movie 6,’ teases ‘equal opportunity offenders’ (exclusive)

Marlon Wayans explains why he slimmed down to play Shorty in Scary Movie 6. The comedian and Him star teases...

Terence Crawford shooting details: The story of boxer’s 2008 near-death experience that ‘changed my life’

Terence Crawford shooting details: The story of boxer’s 2008 near-death experience that ‘changed my life’ originally appeared on The Sporting...

Old MEAC Foe on Deck for Cats Football

Story Links ORANGEBURG, SC. – For the third straight week to open the season, the...

Mizzou-Louisiana football game time changed | Mizzou Xtra

COLUMBIA — The kickoff time for Saturday’s Mizzou football game against Louisiana has been moved to noon due to heat,...

MLB Power Rankings Week 24: Every team’s standing in mid-September

Sep 11, 2025, 07:00 AM ET Almost halfway through September, the 2025 playoff picture is taking shape — but it...

Eric Trump Uses Charlie Kirk’s Death to Sell His Book

Eric Trump has pushed his memoir into the Charlie Kirk conversation by vowing to donate a “portion” of new sales...

Sarah Jessica Parker, Jonathan Groff Host Broadway Luncheon

Sarah Jessica Parker and Tony Award winner Jonathan Groff hosted a luncheon gala on Monday to celebrate 25 years of...

Mariners Next Star? MLB Insider Shares Praise For Top Prospect

The Seattle Mariners have been one of the more intriguing teams to follow this season. They’re loaded with talent, and...

WWE Hall of Famer Suffers Stroke

Scouted selects products independently. If you purchase something from our posts, we may earn a small commission. The way you...

10-year Treasury yield falls to 4% then snaps back as traders assess inflation data

The 10-year U.S. Treasury yield fell to 4% Thursday, then snapped back as investors assessed the latest inflation data, as...

‘What’s Going On Here’: X Users Ask If Trump’s Video After Charlie Kirk Shooting Is AI-Made | World News

Last Updated:September 11, 2025, 10:57 IST As the claims of AI-generated content surfaced, AI-focused WhatsApp groups lit up with debate....

Fox News star Jesse Watters’ wife Emma announces tragic family loss – Celebrity News – Entertainment

The Watters family has endured devastating heartbreak over recent days. Friday night saw Emma, 32, who wed Fox News personality...

Man of Tomorrow Movie Set as Superman Followup for 2027

James Gunn has unveiled the next project in his Superman Saga. Man of Tomorrow will be in theaters July 9,...

Pixel 10 loses ‘Daily Hub’ preview, Google working to improve

On the Pixel 10, Daily Hub brings together your calendar, Magic Cue, and other suggestions. Google is now pausing the...

We Just Got New Updates on Kingdom Hearts 4 and FF7 Remake Part 3

I’m still playing Final Fantasy 7 Rebirth (this backlog is insane), and I’m loving my time with it. While I...

Israel carries out attack against Hamas leadership in Qatar, Israeli source says

Facebook Tweet Email Link Israel carried out an attack against the Hamas leadership in Doha, an Israeli source told CNN,...

‘SmartLess’ Coming to the Hollywood Bowl for Fall Podcast Taping

“SmartLess” is coming to the Hollywood Bowl this fall for what is certain to be one of the most well-attended...

Who has qualified for World Cup 2026? Full list of teams

Clint Dempsey predicts which guys will start for Pochettino in 2026 Former USMNT player Clint Dempsey on Coach Pochettino’s first...

Kelly Ripa, Mark Consuelos Have Black Bathroom with Matching Toilet Paper (Exclusive)

NEED TO KNOW Kelly Ripa and Mark Consuelos revealed in an exclusive interview with PEOPLE that they have a black...

La Casa de los Famosos México en vivo: Facundo es el sexto eliminado del reality show

Facundo revela quiénes son sus favoritos para ganar Después de convertirse en el sexto eliminado, Facundo se presentó en la...

Valkyries first WNBA expansion team to reach playoffs in inaugural season

SAN FRANCISCO — The Golden State Valkyries made history Thursday night as they became the first WNBA expansion franchise to...

Why Ferrari didn’t use Hamilton to help Leclerc

Ferrari has explained why it decided against using Lewis Hamilton to try to tow team-mate Charles Leclerc to pole position...

TIFF 2025: Cillian Murphy’s Steve is a dour, dark delight

The first actor to ever win two consecutive Oscars didn’t exactly break the mould to do so. Spencer Tracy snagged...

Emma Raducanu: British number one withdraws from Billie Jean King Cup

British number one Emma Raducanu has withdrawn from the Great Britain team for this month’s Billie Jean King Cup Finals...

Latest news for Browns rookie

$30 billion expected to be legally wagered on 2025 NFL season Americans are expected to wager an estimated $30 billion...

Luke Fahey outshines Ryder Lyons, Mission Viejo routs Folsom

Ohio State commit Luke Fahey throws for 326 yards on 21 of 31 passes with five touchdowns to lead Mission...

Breaking Down the Mustangs Ahead of Week 2

The Baylor Bears are coming off a disappointing loss to the Auburn Tigers to start the 2025 season. Unfortunately for...

Stock market today: Live updates

Traders work on the floor at the New York Stock Exchange (NYSE) in New York City, U.S., September 3, 2025....

The interstellar comet 3I/ATLAS is wrapped in carbon dioxide fog, NASA space telescope reveals

On July 1, 2025, the Deep Random Survey remote telescope in Chile, part of the ATLAS (Asteroid Terrestrial-impact Last Alert...

Norman Reedus’ son makes alarming threat after arrest for assault

Norman Reedus and supermodel Helena Christensen’s troubled son, Mingus Reedus, asked a startling question one day after he was arrested...

Where Is Paula Deen Now? Inside the Celebrity Chef’s Life After Food Network

NEED TO KNOW It has been over a decade since Paula Deen’s Food Network show came to an end in...

Sydney Sweeney’s ‘Americana’ co-star Halsey slams fans who boycotted film over ‘denim bulls–t’

Sydney Sweeney’s “Americana” co-star Halsey slammed fans who are boycotting their film due to the former’s American Eagle controversy. “you...

Milla Jovovich Gushes Over Paul W.S. Anderson in 16th Wedding Anniversary Tribute

NEED TO KNOW Milla Jovovich and her husband, Paul W.S. Anderson, are celebrating 16 years of marriage with a series...

Ozzy Osbourne ‘knew’ he was dying during final Black Sabbath show

When a “frail” Ozzy Osbourne took the stage for his final Black Sabbath show, he knew the end was coming....

See Photos of Pierce Brosnan, Colin Farrell, Margot Robbie, Anne Hathaway and More

Stars have been everywhere this week, from Pierce Brosnan looking as dapper as ever in London to Margot Robbie and...

Meghan Markle sending ‘intentional’ message to royals with calculated move on Season 2 of Netflix show

Meghan Markle is allegedly sending an “intentional” message to the royals with her fashion choices for Season 2 of her...

Jillian Michaels Slams ‘Egregious’ Claims in ‘The Biggest Loser’ Documentary

NEED TO KNOW Jillian Michaels is denying claims made against her in Netflix’s docuseries Fit for TV: The Reality of...

Joan Collins, 92, defies age in chic white swimsuit on vacation

Age is just a number. Joan Collins flaunted her “timeless beauty” in a chic white swimsuit as she shared a...

See Photos of Kaitlyn Dever, Pedro Pascal, Cynthia Erivo and More

Stars have been everywhere this week. Kaitlyn Dever and Pedro Pascal attend the HBO Max Emmy Nominee Celebration in Hollywood,...

Livvy Dunne talks to Page Six about being a Taylor Swift fan

Gymnast and social media star Livvy Dunne is a certified Swiftie. Dunne, who is dating Pirates All-Star pitcher Paul Skenes,...

Bella Thorne Reacts After Fans Criticized Her for Proposing to Fiancé Mark Emms

NEED TO KNOW Bella Thorne responded after fans criticized her for proposing to her fiancé, Mark Emms, two years after...

Kate Middleton and Prince William’s new home forces 2 families to ‘move out’: report

Kate Middleton and Prince William’s new family mansion reportedly forced two families to move out of their nearby homes. The...

Seth Green Teases a DuJour Reunion from ‘Josie and the Pussycats’

NEED TO KNOW In an interview, Seth Green recently said he would be open to a DuJour reunion DuJour is...

Courtney Stodden takes new swipe at Chrissy Teigen four years after cyberbullying scandal

Courtney Stodden claims she sent a friendly message to Chrissy Teigen, but she’s being “completely ignored” four years after their...

Mila Kunis Says She Barely Ate During Prep for ‘Black Swan’ Role

NEED TO KNOW Mila Kunis is recounting her intense preparation for her role as a professional ballerina in Black Swan...

Gal Gadot says ‘pressure’ to speak out against Israel caused ‘Snow White’ movie to flop

Gal Gadot revealed she believes the “pressure” placed on celebrities to speak against Israel played a role in her Disney...

Peacemaker’s Jennifer Holland on Work-Life Balance in Marriage to Creator James Gunn (Exclusive)

NEED TO KNOW Peacemaker actress Jennifer Holland opens up about the work-life balance in her relationship with series creator James...

Pierce Brosnan reveals the secret behind his great head of hair and aging well

Pierce Brosnan may be unlocking the secret to why Irish men seem to possess enviable mops of hair. “I don’t...

Viola Davis Shares Photos from Her 60th Birthday Celebration Vacation

NEED TO KNOW Viola Davis celebrated her 60th birthday in Cabo San Lucas, Mexico The Oscar-winning actress marked the milestone...

Kate Gosselin snubs estranged son Collin, says her kids ‘all get along’ and have ‘wonderful’ bond

Kate Gosselin gushed over how well her children “get along” after her estranged son, Collin, penned an emotional open letter,...

Johnny Knoxville, 54, Shows Off Buff Arms While Hitting the Speed Bag

NEED TO KNOW Johnny Knoxville showed off his skills — and some serious biceps — on the speed bag in a...

Quinn XCII answers questions about his new album ‘LOOK! I’m Alive’ in Confession Cube

Quinn XCII answers questions about his new album ‘LOOK! I’m Alive’ in Confession Cube Next Previous

Katie Holmes Wore a Flannel with Trousers, Shop the Look

Welcome to The Blueprint, where we break down the celebrity looks we want to wear right now and build them...

Dua Lipa flaunts her abs during paddleboard yoga in Ibiza

Dua Lipa is showing off her impressive abs and athletic ability in Ibiza. The singer, 29, was snapped doing yoga...

Does Kim Cattrall Return as Samantha?

Warning: This story contains spoilers for the And Just Like That… series finale. NEED TO KNOW Fans have been wondering...

Olivia Jade Giannulli is the spitting image of mom Lori Loughlin in first sighting since Jacob Elordi split

Like mother, like daughter. Olivia Jade Giannulli looked like her mom Lori Loughlin’s twin in her first sighting since her...

How Prince William, Prince Harry Impact Diana’s Causes 28 Years After Her Death

NEED TO KNOW Prince William and Prince Harry are separately backing causes that Princess Diana championed during her life Tessy...

Taylor Swift details emotional moment that left her and Travis Kelce ‘weeping’

Travis Kelce comforted Taylor Swift as she fought back tears while discussing the dramatic moment she found out she would...

Taylor Swift Reflects on Taking Care of Her Dad After His Heart Surgery

NEED TO KNOW Taylor Swift opened up about her dad Scott Swift’s major quintuple bypass surgery Swift revealed she moved...

Taylor Swift’s new album ‘Life of a Showgirl’: Everything to know

Taylor Swift sent shockwaves through her fandom by announcing her 12th studio album during her debut appearance on boyfriend Travis...

Luke Bryan Slams ‘Idiots’ Throwing Objects at Musicians During Concerts

NEED TO KNOW Luke Bryan has some words for “idiots” who throw objects at musicians during shows In July, the...

Taylor Swift gets cozy with Travis Kelce and teases ‘male sports fans’ in ‘New Heights’ preview

Taylor Swift gets cozy with Travis Kelce and teases ‘male sports fans’ in ‘New Heights’ preview Next Previous

Naomi Watts Wore Wide-Leg Jeans Like These Pairs from Amazon

Celebrities have been reaching for roomy, breezy pants all summer long — and it doesn’t look like the comfortable trend...

Blake Lively takes swipe at Justin Baldoni’s lawyer over alleged ‘smear campaign’ in deposition transcript

Blake Lively took a swipe at Justin Baldoni’s lawyer, Bryan Freedman, during her July 31 deposition, accusing him of being...

Jessica Alba Wore a Cardigan and Trousers, Get the Look

Welcome to The Blueprint, where we break down the celebrity looks we want to wear right now and build them...

Dua Lipa celebrates 30th birthday in sequin dress with a butt cutout

Dua Lipa celebrated her 30th birthday early in a custom white dress with a butt cutout. Instagram/dualipa Bootylicious. Though Dua...

Taylor Swift Announces New Album The Life of a Showgirl with Help from Travis and Jason Kelce

NEED TO KNOW Taylor Swift has revealed her next era will be The Life of a Showgirl The announcement came...

Taylor Swift announces new album ‘Life of a Showgirl’ on ‘New Heights’ podcast

Drop everything now! Taylor Swift announced she’s releasing new music during a surprise appearance on her boyfriend Travis Kelce’s “New...

Bethenny Frankel Admits She’s Currently ‘Afraid’ to Date

NEED TO KNOW Bethenny Frankel opened up about her dating life in a candid TikTok In the video, Frankel shares...

Lauren Sánchez marks a major parenting milestone as son Evan goes to college

Lauren Sánchez felt “proud,” but also “heartbroken,” as she dropped her son, Evan Whitesell, off at college. The former journalist...

Jennifer Aniston Makes Rare Comments About Her Divorce from Brad Pitt

NEED TO KNOW Jennifer Aniston gave some rare comments about her divorce from Brad Pitt in her newly published September...

Exes Joe Jonas and Demi Lovato reunite for ‘Camp Rock’ performance

The band is all here. Exes Joe Jonas and Demi Lovato stunned fans when they reunited for a “Camp Rock”...

Maluma Stops Concert to Scold Mom Who Brought Baby

NEED TO KNOW Maluma called out a fan for bringing a baby to his Mexico City concert “Do you think...

Kathy Griffin confirms third facelift after raising eyebrows with ‘very taut’ appearances

Kathy Griffin confirmed she underwent a third facelift after making headlines due to her recent public appearances. The 64-year-old comedian...

Singer Says He’ll ‘Never Play in Kansas City’

NEED TO KNOW Zach Bryan said he “will never play in Kansas City” while feuding with Kansas City Chiefs fans...

‘Doomsday prepper’ Josh Duhamel reveals ‘calling’ that made him leave LA for Minnesota

Livin’ life in the “Land of 10,000 Lakes.” “Doomsday prepper” Josh Duhamel revealed that he was inspired to leave Los...

Linda Hamilton Is ‘Uncomfortable’ with Praise, Being Told She’s an ‘Icon’ (Exclusive)

NEED TO KNOW Linda Hamilton sometimes ran into a starstruck response while on set for her new film Osiris, she...

Kate and Jon Gosselin’s son Collin pens message to estranged siblings

Kate and Jon Gosselin’s son Collin released an emotional open letter to his seven siblings. The “Jon & Kate Plus...

‘TMNT’ Co-Creator Reveals Which Actor Wants to Play Casey Jones (Exclusive)

NEED TO KNOW Teenage Mutant Ninja Turtles co-creator Kevin Eastman said that actor Joe Manganiello would like to play Casey...

‘DWTS’ alum Cheryl Burke reveals how she dropped 41 pounds

Cheryl Burke lost a significant amount of weight — while still enjoying the sweeter things in life. “At my heaviest...

Melissa McCarthy and Husband Ben Falcone Recreate ‘Ghost’ Pottery Scene

NEED TO KNOW Melissa McCarthy and husband Ben Falcone visited Wild Clay L.A. on Friday, Aug. 8 They shared a...

Katy Perry shows off brutally scraped knees she sustained during ‘Lifetimes’ tour

She’ll cry about it later. Katy Perry showed off her brutally scraped knees she sustained while dancing on her “Lifetimes”...

Lindsay Lohan Shares ‘Parent Trap’ Reunion Selfie with Elaine Hendrix

NEED TO KNOW Lindsay Lohan shared a new selfie with her Parent Trap costar Elaine Hendrix from behind-the-scenes of Freakier...

Kylie Jenner rocks tiny bikini top ahead of 28th birthday

Kylie Jenner is celebrating her last few days as a 28-year-old in a stylish little black bikini top. The makeup...

Anderson Cooper Shocks Fans with Unrecognizable Gray Facial Hair

NEED TO KNOW Anderson Cooper surprised fans with a new look in his latest Instagram update On Aug. 7, the...

‘Virtual Reali-Tea’ unpacks Tamra Judge’s break down over Teddi’s fall in New Orleans

‘RHOC’ recap: ‘Virtual Reali-Tea’ unpacks Tamra Judge’s break down over Teddi’s fall in New Orleans Next Previous

Heather and Tarek El Moussa’s Son Tristan, 2, Is Growing Up Fast in New Photos

NEED TO KNOW Heather and Tarek El Moussa’s 2-year-old son Tristan is preparing for preschool HGTV star Heather shared a...

Jack Nicholson’s grandson Sean arrested for domestic violence: report

Jack Nicholson’s grandson Sean was reportedly arrested on felony domestic violence charges in Los Angeles. Sean Knight Nicholson, 29, was...

‘The White Lotus’ Star Sam Nivola Addresses Nepo Baby Label

NEED TO KNOW Sam Nivola addressed the nepo baby label in a new interview and said his success is “sometimes...

Kelly Clarkson’s ex-husband, Brandon Blackstock, dead at 48 after cancer battle

Kelly Clarkson’s ex-husband, Brandon Blackstock, has reportedly died after battling cancer. He was 48. “It is with great sadness that...

Heidi Klum Teases Her ‘Extra Ugly’ and ‘Super Scary’ Halloween Costume

NEED TO KNOW During an appearance on The Tonight Show Starring Jimmy Fallon Wednesday, Aug. 6, Heidi Klum began teasing...

Kelly Clarkson abruptly cancels Las Vegas residency shows for the second time

Kelly Clarkson canceled her remaining Las Vegas residency dates in August. Getty Images for Live Nation Las Vegas Pop icon...

Jeff Bezos and Lauren Sánchez Bezos Hit the Dance Floor in Ibiza

NEED TO KNOW Jeff Bezos and Lauren Sánchez Bezos were spotted vacationing in Spain on their extended European honeymoon The...

Nordstrom has great deals on New Balance sneakers right now

Page Six may be compensated and/or receive an affiliate commission if you click or buy through our links. Featured pricing...

Melinda French Gates Remembers Serena Williams Hyping Her Up When She Thought Nothing Would Fit Her Body

NEED TO KNOW Melinda French Gates credited Serena Williams for boosting her body confidence when speaking with her during a...

Why Michelle Obama fought ‘first sparky feelings’ when she met ‘sexy’ Barack

Michelle Obama took “IMO” listeners down memory lane on Wednesday. The former first lady kicked off the podcast episode by...

Step by Step’s Angela Watson and Husband Share Updates on Baby James

NEED TO KNOW Angela Watson and her husband Brian Nahas share updates on their son James after welcoming the baby...

Shirtless Orlando Bloom shows off jacked body at the beach

Life’s a beach — and newly single Orlando Bloom is just playing in the sand. The shirtless actor flaunted his...

Woody Allen Compared Jeffrey Epstein to Dracula in Birthday Letter

NEED TO KNOW The New York Times reported a letter written by Woody Allen to Jeffrey Epstein in 2016 The...

Brad Pitt gets into character while filming in LA and more star snaps

Brad Pitt films in LA, Lin-Manuel Miranda meets his wax figure and more snaps…

All About Joely, Carlo and Natasha

Vanessa Redgrave is part of a British acting dynasty that spans more than five generations — and includes her three...

Christie Brinkley, 71, and daughter Sailor, 27, matched with the same men on dating app

Christie Brinkley and her look-alike youngest daughter, Sailor Brinkley Cook, attract the same men despite their 44-year age difference. The...

Justin Timberlake Jokes He’s ‘Not Doing S— Today’ After Tour Ends

NEED TO KNOW Justin Timberlake is “not doing s—” as he relaxes at home, following the end of his two-year...

Brandi Glanville names her facial parasite after her ‘Real Housewives’ nemesis

Brandi Glanville named her facial parasite “Caroline,” the same name as her “Real Housewives” nemesis, Caroline Manzo. The “Real Housewives...

Dylan Dreyer Marks ‘Surprise’ Birthday Party with Hoda Kotb and Kids

NEED TO KNOW Dylan Dreyer shared a glimpse at her “surprise” 44th birthday party to social media The Today meteorologist...

Mila Kunis and Ashton Kutcher show PDA at Backstreet Boys concert

They want it that way. Mila Kunis and Ashton Kutcher showed rare PDA while enjoying the Backstreet Boys’ larger-than-life “Into...

Erik Menendez Returns to Prison After Being Hospitalized, Undergoing Surgery

NEED TO KNOW Erik Menendez has returned to prison after being hospitalized to receive treatment for kidney stones Erik’s stepdaughter,...

Oasis ‘shocked’ after man falls to his death at London concert

Oasis has spoken out after a man fatally fell from the upper level at their Wembley Stadium show. “We are...

Elizabeth Holmes Works Out in Texas Prison amid 11-Year Fraud Sentence: Photos

NEED TO KNOW Elizabeth Holmes was photographed working out in prison on Aug. 2 The disgraced former tech CEO is...

Travis and Jason Kelce’s dad Ed’s girlfriend, Maureen Maguire, dead at 74

Ed Kelce’s girlfriend, Maureen Maguire, has died. She was 74. According to an obituary the father of NFL stars Travis...

Meryl Streep and Stanley Tucci Film ‘The Devil Wears Prada 2’ in N.Y.C.: Photos

NEED TO KNOW Meryl Streep and Stanley Tucci are on set for the filming of The Devil Wears Prada 2...

Eva Longoria rocks white bikini and sheer romper in Spain

Eva Longoria rocked a skimpy white bikini and a sheer romper during a family getaway in Marbella, Spain, this week....

Brooklyn Beckham and Nicola Peltz Renew Their Vows 3 Years After Wedding (Exclusive)

NEED TO KNOW Brooklyn and Nicola Peltz Beckham renewed their wedding vows on Saturday, Aug. 2 The vow renewal celebration...

Vanessa Hudgens, Jennifer Lopez, Nick Jonas and more

Star snaps of the week: Vanessa Hudgens, Jennifer Lopez, Nick Jonas and more Vanessa Hudgens pauses while on a babymoon...

‘They Have a Lot in Common’ (Exclusive)

NEED TO KNOW Justin Trudeau and Katy Perry sparked romance rumors in recent days by spending time together in Montréal...

Padma Lakshmi rocks hot pink string bikini in the Hamptons

Padma Lakshmi modeled a tiny hot pink string bikini after revealing a substantial change in her bra size. In the...

‘Naked Gun’ Director Limited Reboot to Only 1 O.J. Simpson Joke to Be ‘Respectful’

NEED TO KNOW Akiva Schaffer is directing the latest iteration of the popular police movie, The Naked Gun The comedy...

Justin Timberlake, Bella Hadid, more

Justin Timberlake recently revealed in a lengthy Instagram statement that he has been diagnosed with Lyme disease. Unfortunately, the pop...

Pregnant Wife of Former NBA Star Attacked by Shark

NEED TO KNOW Eleonora Boi opened up about getting bit by a shark in Puerto Rico on her Instagram The...

Kim Zolciak cops to spending daughters Ariana and Brielle’s money on ‘WWHL’

Kim Zolciak finally addressed spending her daughters’ money, one month after Ariana Biermann called her out. On Thursday’s episode of...

Jason Momoa Calls His Dad’s Cameo in ‘Chief of War’ a ‘Pretty Beautiful Moment’

NEED TO KNOW Jason Momoa’s dad plays a special role in his life and in his upcoming AppleTV+ series The...

Tyra Banks confesses ‘disgusting and erotic’ addiction

Tyra Banks knows how to pick ’em. The supermodel revealed her “disgusting and erotic” habit of popping pimples and picking...

Jesse Metcalfe Reveals How His Girlfriend Reacted to Ex Scheana Shay’s Book Detailing Their Past Romance (Exclusive)

NEED TO KNOW Jesse Metcalfe revealed how girlfriend Helene Immel reacted to Scheana Shay detailing their brief relationship in her...

Alix Earle shares update on her acne battle and current skincare routine

Page Six may be compensated and/or receive an affiliate commission if you click or buy through our links. Featured pricing...

See Photos of Jenna Ortega, Pamela Anderson, Liam Neeson and More

Stars have been everywhere this week. In London, Jenna Ortega is a vision of gothic beauty at the premiere of...

Adam Carolla claims ‘mean’ Ellen DeGeneres made staff ‘scared to death’

Comedian Adam Carolla claimed Ellen DeGeneres’ daytime talk show staff members were “scared to death” of her and “cowering” when...

Kelly Clarkson’s Sideboard Is 73% Off at Wayfair

Kelly Clarkson kicked off her Las Vegas residency on July 11, and we can’t help but fawn over her recording...

Stuart Weitzman shoes are on sale for up to 87% off at Nordstrom Rack

Page Six may be compensated and/or receive an affiliate commission if you click or buy through our links. Featured pricing...

All About Klay Thompson’s Parents, Mom Julie and Dad Mychal Thompson

NEED TO KNOW Klay Thompson was born to Mychal and Julie Thompson on Feb. 8, 1990 His mom, Julie, was...

-

Finance & Banking1 day ago

Retiring Next Year? Discover the Right Monthly Income Target

-

Finance & Banking2 days ago

Earnings From Nvidia, Home Depot, Banks, and Berkshire; Trump Speech

-

Entertainment2 days ago

Tim McGraw reveals most controversial song Indian Outlaw after industry tried to cancel hit

-

Trending2 days ago

Momentos históricos de tormentas de nieve en Nueva York – Telemundo New York (47)

-

Entertainment1 day ago

Jennifer Lopez celebrates twins Emme and Max’s 18th birthday with sweet tribute

-

Finance & Banking20 hours ago

How Much Are Americans Saving? A Look at Bank Balances

-

Entertainment14 hours ago

Kylie Jenner looks visibly uncomfortable at Alan Cumming’s cheeky joke at BAFTAs

-

Finance & Banking10 hours ago

Major Indexes Plunge Amid Tariff Uncertainty; Dow Sheds 800 Points; Bitcoin Drops, Safe-Haven Gold Rises